Test Owner

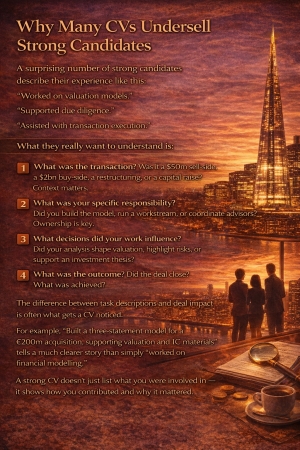

Why Many CVs Undersell Strong Candidates

A surprising number of strong candidates describe their experience like this:

“Worked on valuation models.”

“Supported due diligence.”

“Assisted with transaction execution.”

The issue is that while all of this may be true, it doesn’t tell hiring managers very much.

At the CV screening stage, especially in private equity, credit, and advisory roles, hiring managers are trying to quickly understand what you’ve actually done and the level at which you operate. Generic descriptions make it difficult to distinguish one candidate from another.

What they really want to understand is:

1. What was the transaction?

Was it a $50m sell-side, a $2bn buy-side, a restructuring, or a capital raise? Context matters.

2. What was your specific responsibility?

Did you build the model, run a workstream, or coordinate advisors? Ownership is key.

3. What decisions did your work influence?

Did your analysis shape valuation, highlight risks, or support an investment thesis?

4. What was the outcome?

Did the deal close? At what value? What was achieved?

The difference between task descriptions and deal impact is often what gets a CV noticed.

For example, “Built a three-statement model for a €200m acquisition, supporting valuation and IC materials” tells a much clearer story than simply “worked on financial modelling.”

A strong CV doesn’t just list what you were involved in — it shows how you contributed and why it mattered.

Often, candidates already have the right experience. It’s just not being communicated clearly.

And in many cases, a relatively small rewrite can be the difference between being overlooked and getting the interview.

If you’re considering a move or want a second opinion on how your experience is coming across, Circle Square works closely with candidates to refine CVs and position their experience in a way that resonates with investment teams. We’re always happy to share feedback on what’s working in the current market and how to maximise your chances of getting in front of the right opportunities.

The difference between a good deal team and a great one

Technically strong deal teams are common.

But the teams that consistently produce the best results often share a few characteristics:

1️⃣ Clear ownership of workstreams

2️⃣ Open debate around investment decisions

3️⃣ Junior team members encouraged to challenge assumptions

4️⃣ Seniors willing to explain how they think about deals

It creates an environment where people learn quickly and improve each investment process.

Over time, that culture compounds.

And it’s often the reason some firms consistently outperform others.

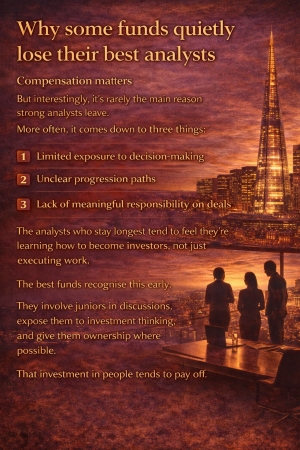

Why some funds quietly lose their best analysts

Compensation matters.

But interestingly, it’s rarely the main reason strong analysts leave.

More often, it comes down to three things:

Limited exposure to decision-making

Unclear progression paths

Lack of meaningful responsibility on deals

The analysts who stay longest tend to feel they’re learning how to become investors, not just executing work.

The best funds recognise this early.

They involve juniors in discussions, expose them to investment thinking, and give them ownership where possible.

That investment in people tends to pay off.

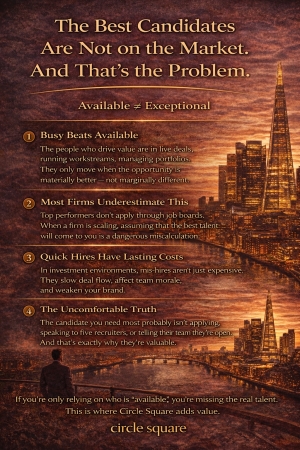

The Best Candidates Are Not on the Market. And That’s the Problem

If you’re only hiring people who are actively applying, you’re fishing in the shallow end.

The strongest Associates, VPs and Directors in M&A, Private Equity, Credit and Tech advisory are not updating their CVs.

1. They’re executing.

2. They’re trusted.

3. They’re being promoted.

And they’re not browsing LinkedIn jobs at 10pm. Yet many hiring processes still revolve around who’s “available.”

Available does not equal exceptional.

Busy beats available

When we map a market properly, the pattern is obvious:

The people who drive value are:

- In live deals

- Running workstreams

- Managing portfolios

- Being relied upon internally

- They’re not frustrated.

- They’re not desperate.

- They’re not sending their CV to five recruiters.

- They’re selective.

- And they only move when the opportunity is materially better — not marginally different.

Most firms underestimate this

There’s a dangerous assumption in growth phases: “If the platform is good, the best people will apply.”

They won’t.

Top performers need:

- A clear strategic story

- Genuine responsibility

- Cultural alignment

- Long-term upside

Comp alone rarely moves them. Title inflation doesn’t move them either. What moves them is trajectory.

The hidden cost of a “quick” hire

When firms scale — new fund, new strategy, new vertical — speed becomes the priority.

But in investment environments, a mis-hire isn’t just expensive.

It impacts:

- Deal quality

- Execution speed

- Internal morale

- LP perception

- Your reputation in a tight talent market

The wrong Associate can slow a team down.

The wrong VP can create invisible friction for years.

And undoing it is rarely quick.

The uncomfortable truth

The best candidate for your role probably:

- Isn’t applying

- Isn’t speaking to multiple recruiters

- Hasn’t told their team they’re open

- And doesn’t “need” to move

They need to be approached properly;

- With credibility.

- With context.

- With discretion.

- That takes work.

It takes targeted mapping, informed conversations and a clear articulation of why your platform is genuinely better — not just different.

Why this is where Circle Square adds value

At Circle Square, we don’t rely on inbound flow or broad advertising.

- We map markets properly.

- We identify the outperformers.

- We approach selectively and credibly.

Because we operate exclusively across M&A, Private Equity, Family Office and Credit, we understand the nuance of platform quality, fund cycles, team dynamics and what genuinely motivates top performers to move.

If you’re building a team and want access to the people who aren’t on the market — but should be on your radar — let’s have a conversation.

The difference between available talent and exceptional talent is rarely luck. It’s approach.

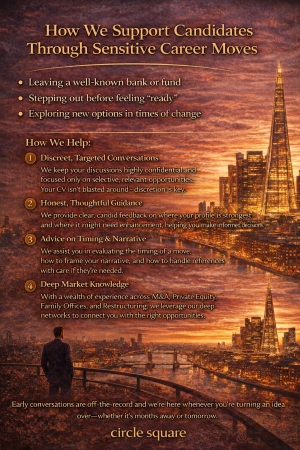

How we support candidates through sensitive career moves

- Moving from a well‑known bank or fund where news travels fast

- Stepping out of a role that no longer fits, before you feel “ready”

- Exploring options while your current platform is going through change

- Keeping conversations quiet and targeted, not sending your CV everywhere

- Being honest about where your profile is strongest – and where it isn’t

- Helping you think through timing, narrative and references, not just comp

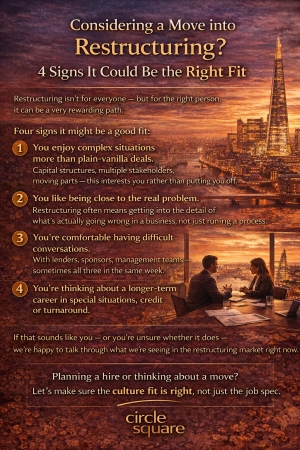

Considering a move into restructuring? 4 signs it could be the right fit

Restructuring isn’t for everyone – but for the right person, it can be a very rewarding path.

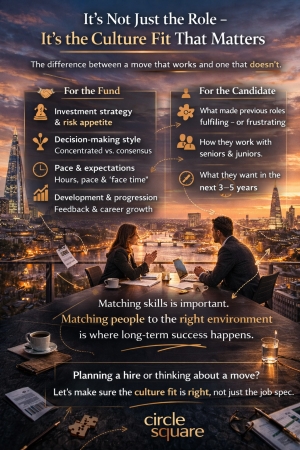

Why we spend so much time understanding a fund’s culture

- Investment strategy and risk appetite

- Decision‑making style – concentrated vs. consensus

- Expectations around hours, pace and “face time”

- Approach to development, feedback and progression

- What has made previous roles fulfilling or frustrating

- How they like to work with seniors and juniors

- What they want their next 3–5 years to look like

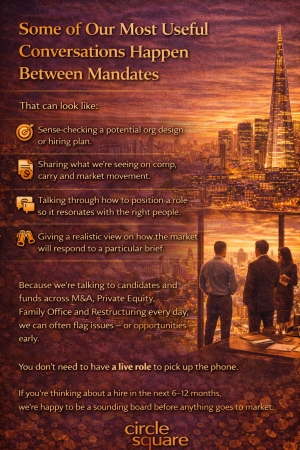

How we partner with clients between mandates

- Sense‑checking a potential org design or hiring plan

- Sharing what we’re seeing on comp, carry and market movement

- Talking through how to position a role so it resonates with the right people

- Giving a realistic view on how the market will respond to a particular brief

The candidates your process is missing (and why)

- A job spec that’s really just the CV of the last hire, not what you need now

- Over‑indexing on one type of background, rather than the skills the role needs

- Processes that are so long or unclear that strong candidates simply opt out

- People who bring a slightly different angle (e.g. more portfolio, more restructuring, more sector depth)

- Candidates who might have one or two non‑standard points in their CV, but a clear story

- Individuals who perform better in practical, conversation‑led interviews than formal panels

Gaps, Quiet Periods & Softer Deal Flow: How to Own Your Narrative

Not every CV is a straight line of back‑to‑back live deals.

Most hiring managers know this – but they do want a clear, confident story.

If you have a gap, a quieter period for deal flow, or slightly softer experience:

- Own it early. Don’t wait for an interviewer to drag it out of you.Explain the context – market conditions, team changes, internal moves – without blaming.

- Focus on what you learned and did during that time (skills, responsibilities, preparation for the next step).

- Be clear about why you’re now ready for this role, not still processing the lastc one. The goal isn’t a perfect narrative – it’s a credible, honest one.

We spend a lot of time with candidates across M&A, Private Equity, Family Office and Restructuring helping them shape that story.

If this resonates and you’d like a second opinion on how you’re positioning your experience, we’re happy to help.