Test Owner

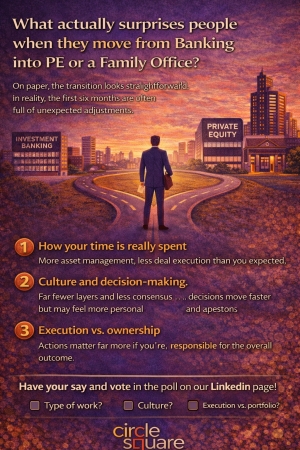

What actually surprises people when they move from Banking into PE or a Family Office?

On paper, the jump from Investment Banking into Private Equity or a Family Office looks straightforward.

In reality, the first six months often feel very different from what people expect.

We speak to candidates every week who have already made the move — and a common theme comes up:

the biggest surprises are rarely about technical skill.

They tend to fall into three broad areas.

1. How your time is really spent

Many bankers expect to spend most of their time on new deals. In practice, the mix is often very different — with far more time going into asset management, portfolio reviews, refinancing, reporting, or working with operating partners than expected.

For some people, that’s a welcome shift. For others, it feels very different from the “deal-driven” image they had in mind.

2. Culture and decision-making

Moving from a large institution into a fund — or especially into a Family Office — can be a shock to the system.

Fewer layers, more direct accountability, and far less consensus-building means decisions move faster… but they also feel more personal.

What feels like freedom to one person can feel like ambiguity to another.

3. Execution vs. ownership

In PE and Family Offices, you don’t just run processes — you live with the outcomes.

Whether it’s a lease-up, a refinancing, a bolt-on acquisition or an exit, you feel the result far more directly than you ever did in banking.

That shift in ownership is energising for many — but it’s also a big adjustment.

We’re curious to hear from people who have actually made the move.

If you’ve gone from Investment Banking into PE or a Family Office, what surprised you most in your first six months?

???? Head to our LinkedIn page to vote in the poll and (if you’re comfortable) share your experience in the comments. www.linkedin.com/company/circle-square-talent

The patterns that emerge from these conversations are often far more helpful to candidates than any job description.

Why more PE and Banking professionals are quietly exploring Family Offices

Not every good investment career has to follow the same track.

We’re seeing a growing number of bankers and PE professionals taking a serious look at Family Offices — not because they’re disillusioned, but because their priorities are evolving.

What’s driving that interest?

???? Closer proximity to capital

Working directly with principals rather than committees means ideas move faster and relationships matter more.

???? A longer investment horizon

Many Family Offices invest with generational capital, allowing for more patient underwriting and less pressure to exit on someone else’s timetable.

???? A broader mandate

Alongside direct deals, many roles include co-investments, public markets, and sometimes operating or strategic projects that wouldn’t sit inside a typical fund.

That said, Family Offices aren’t a shortcut — they’re simply a different path.

The things that matter most in FO careers are often underestimated:

• Alignment with the principal — values, risk appetite, and how decisions get made

• Comfort with fewer layers — less structure, but more personal accountability

• A quieter profile — but often with greater influence on capital and strategy

At Circle Square, we spend a lot of time helping candidates compare PE, Family Office, and other alternatives — not from theory, but from live hiring mandates and real conversations with principals.

If you’re starting to think about what the next 5–10 years of your career should look like, we’re always happy to share what we’re seeing — off the record and without any pressure.

Banking to buyside: the 5 CV tweaks that actually matter

If you’re moving from banking to the buyside, your CV doesn’t need to be clever – it needs to be clear.

Five tweaks that make a real difference:

1️⃣ Lead with deal experience, not responsibilities.

List 3–5 key transactions with your role, size, sector and outcome.

2️⃣ Be explicit about what you owned.

Did you run a workstream, build the model, lead parts of DD? Say so in plain English.

3️⃣ Quantify where you can.

If you helped drive a process to signing in 8 weeks, or supported multiple live deals at once, make that tangible.

4️⃣ Cut the jargon.

Your reader knows the technical language – they just don’t want to work to decode it.

5️⃣ Keep it to two pages or less.

More pages rarely equal more impact.

We review hundreds of CVs a month across M&A, Private Equity, Family Office and Restructuring.

If you’d like an honest view on whether yours is doing you justice, we’re happy to help.

Behind the Scenes of a Smooth PE Hire

What Really Matters Most When You're Considering Your Next Move?

We often hear that compensation, title, and brand name are the top priorities when candidates start thinking about a career move.

But once we’re deep into a hiring process — having real, honest conversations — a different story often emerges.

So we’re asking:

If you had to pick just one factor that matters most to you, what would it be?

-

???? Compensation

-

???? Culture & People

-

???? Carry / Long-Term Upside

-

???? Career Progression & Learning

???? Vote now on our LinkedIn poll and let us know where you stand:

???? Click here to vote

We’d also love to hear the why behind your choice — especially if your priorities have changed over time. Drop your thoughts in the comments.

Final-Round Interviews: Ask the Right Questions Before You Sign

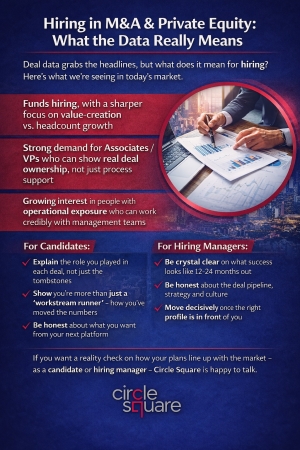

Hiring In M&A and Private Equity; What The Data Really Means

- Funds still hiring, but with a sharper focus on value‑creation vs. headcount growth

- Strong demand for Associates / VPs who can show real deal ownership, not just process support

- Growing interest in people with operational exposure who can work credibly with management teams

- Explain clearly your role on each deal, not just the tombstones

- Show how you’ve helped to move the numbers, not only run workstreams

- Talk honestly about what you want from your next platform

- Crystal clear about what success looks like 12–24 months out

- Honest about the deal pipeline, strategy and culture

- Willing to move decisively once the right profile is in front of them

Launching our PE, M&A, Family Office & Restructuring series

- What we’re hearing from funds and advisory firms about demand and deal flow

- Practical career advice for people thinking about a move (or their next move)

- Honest views on what makes a good hiring process in a competitive market

- A small number of featured, anonymised roles we’re working on

M&A, Venture & Private Equity in MENA: A Market in Motion

Introduction

There’s a quiet confidence building across the Middle East and North Africa (MENA) investment landscape. From family offices to sovereign wealth funds, venture investors to PE houses, the region is seeing a transformation — not just in capital flows, but in deal sophistication, international reach, and appetite for talent.

At Circle Square, we've been closely tracking the evolution of M&A and private capital in the region — and here’s what we’re seeing on the ground.

The Rise of Regional M&A

The last 24 months have seen a notable increase in intra-regional M&A activity, particularly in sectors aligned with national transformation plans — including tech, healthcare, education, logistics, and renewable energy.

Key drivers:

- Government-backed consolidation strategies (particularly in Saudi Arabia and the UAE)

- Cross-border appetite from listed and private companies to scale beyond home markets

- Increased advisory sophistication, with international boutiques and Big Four teams doubling down on MENA

We're seeing a steady rise in junior and mid-level M&A hiring as firms look to bolster their execution capabilities in Riyadh, Dubai, and Doha.

Venture Equity – Resilience & Reset

Venture activity in MENA is going through a natural correction phase, but it’s far from quiet. Saudi’s PIF-backed accelerators and UAE-based family offices remain active — but are increasingly focused on unit economics, governance, and scalability.

Despite the global VC slowdown, capital is flowing into:

- AI, fintech, healthtech and infrastructure-linked tech

- Series A–C stage rounds, with more structured and strategic participation

- Locally backed ventures that align with Vision 2030 and diversification mandates

This has created demand for professionals with transaction experience in both developed and emerging markets — and a hybrid mindset that can bridge start-up agility with institutional expectations.

Private Equity: Local Funds Go Global

MENA-based private equity is in a transition phase — moving from opportunistic investing to long-term platform building. SWFs like Mubadala, ADQ and PIF continue to lead the charge, often co-investing with global partners or launching thematic funds in:

- Healthcare & Pharma

- Digital infrastructure

- Consumer & retail consolidation

- Real estate and logistics

At the same time, regional funds are professionalising internally. There’s more emphasis on building permanent capital teams — origination, execution, and portfolio management — especially those with international experience and Arabic cultural fluency.

What It Means for Talent

In short, the market is maturing — and talent demand is rising fast.

We’re seeing:

- Firms hiring outside the region, with relocation packages and long-term incentive plans

- Diaspora professionals returning, often for strategic leadership roles

- Growing interest in mid-level dealmakers (Associate to VP) who bring structure, hustle, and cultural alignment

Conculsion

For candidates and firms alike, the opportunity is real — but the competition is rising. In MENA, as in other growth regions, the edge goes to those who move early, stay agile, and hire smart.

If you’re thinking of making a move to MENA, building out a deal team or want to discuss the current hiring landscape across PE, venture, or advisory, reach out to us directly on 020 7492 0700 — we’d be happy to talk through what we’re seeing in the market.

5 Questions You Must Nail in a Venture Capital Interview

Introduction

Venture capital interviews go beyond financial acumen—they test your judgment, curiosity, and ability to think like an investor. Whether you’re applying to a seed-stage fund or a multibillion-dollar growth investor, here are five questions that come up again and again—and how to approach them.

1. “What’s a startup you’d invest in and why?”

Pick a real company—not a cliché—and walk through your investment thesis. What problem does it solve? How big is the TAM? Who are the competitors? Bonus points if you’ve spoken with customers or founders.

2. “What makes a great founder?”

You’re not just backing ideas—you’re backing people. VCs look for resilience, storytelling, and domain expertise. Share examples of traits you admire, and ideally, reference founders you've met or studied.

3. “How would you source deals?”

VCs want hungry, well-networked associates. Talk about how you’d tap into founder communities, leverage data, or build your own thesis-driven sourcing pipeline. Show that you’re proactive—not just reactive.

4. “What are the risks in your investment pick?”

This is a test of self-awareness. All startups carry risk—product, team, market timing. A strong candidate doesn’t ignore red flags; they flag them early and explain how they’d mitigate them.

5. “Explain a recent VC deal you found interesting”

Pick one that suits the stage and sector of the fund. Explain the valuation, the round structure, and why the investor led it. Be ready to critique the deal too—politely and thoughtfully.

Conclusion

VC interviews are about pattern recognition and conviction. At Circle Square, we help candidates sharpen their thinking, build credibility, and tell stories that resonate with investors.